Planning to upgrade your kitchen, add a bathroom, or tackle long-overdue repairs? Before you start swinging the hammer, it’s smart to get clear on how you’ll finance the work.

This guide breaks down the most common borrowing options for home renovations – including HELOCs, home equity loans, equity-sharing, and personal loans – and how to choose what’s best for your project and budget.

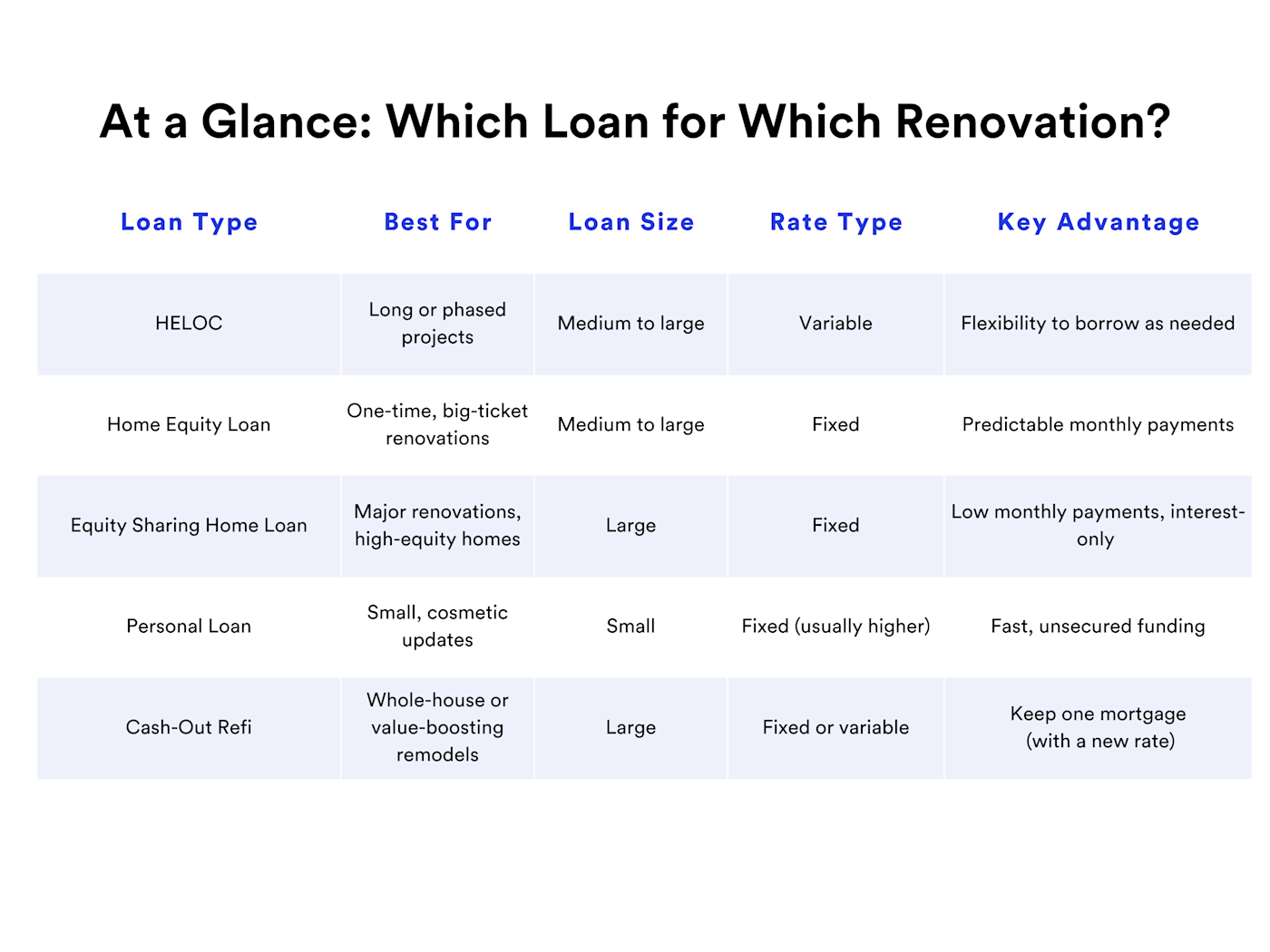

At a Glance: Which Loan for Which Renovation?

HELOC: Flexible Funding Over Time

Best for: Projects with rolling costs, like a basement remodel or multi-stage addition.

A Home Equity Line of Credit (HELOC) works like a credit card backed by your home. You draw funds as needed during the “draw period” (often 5-10 years), then repay over time.

Benefits:

Only pay interest on what you use

Good for uncertain or flexible budgets

Often has a lower starting rate than personal loans

Considerations:

Variable interest rate may rise over time

Requires discipline to avoid overborrowing

Repayment period often brings higher monthly costs

Tip: HELOCs are ideal if your project is spread out, but be aware that your rate (and payment) could jump after the draw period ends.

Home Equity Loan (Second Mortgage): Fixed and Predictable

Best for: Large, one-time renovations with a clear budget.

A home equity loan provides a lump sum with a fixed rate, repaid over a set term. It’s essentially a second mortgage.

Benefits:

Fixed interest and steady payments

Ideal for major upgrades like kitchen or roof replacements

Easier to budget and plan

Considerations:

Higher closing costs than a HELOC or personal loan

You pay interest on the full amount, whether or not you use it all

Tip: This is a great choice if you have a detailed project estimate and want payment predictability.

Equity Sharing Home Loans: A Monthly-Payment Alternative

Best for: Homeowners with significant equity who want to borrow for large-scale upgrades – and prefer lower monthly payments than traditional loans.

An equity sharing home loan, like that offered by Unison, is a second mortgage with a fixed, often lowered interest rate and monthly interest-only payments. What makes it different is the shared appreciation feature: in exchange for lower borrowing costs, Unison receives a portion of the increase in your home’s future value when you sell or refinance.

Benefits:

Fixed interest rate with predictable monthly payments

Lower monthly payments than typical home equity loans or HELOCs

Does not replace your primary mortgage

Considerations:

You’ll give up a portion of future home value gains

The loan must be repaid (plus appreciation share) when you sell or refinance

May not be ideal if you plan to keep your home long-term without selling

Tip: This option can be a strategic fit if you need to fund major home improvements but want to preserve cash flow. Be sure to weigh the long-term cost of shared appreciation.

Personal Loans: Quick Cash for Small Projects

Best for: Cosmetic upgrades or DIY-friendly renovations under $20,000.

Personal loans are unsecured and don’t tap your home’s equity. But they often come with higher rates and shorter repayment terms.

Benefits:

Fast approval and funding

No home equity required

Good for smaller, lower-cost updates

Considerations:

Higher interest rates than equity-based options

Shorter repayment terms can increase monthly payments

Tip: Great for painting, flooring, or appliance upgrades, but not ideal for structural or full-room remodels.

Cash-Out Refinance: Refresh Your Mortgage, Fund Your Project

Best for: Full-home remodels – or when refinancing makes financial sense anyway.

With a cash-out refinance, you replace your current mortgage with a new, larger one, and pocket the difference in cash to fund your renovations.

Benefits:

Potentially lower mortgage rate (depending on market)

Keep to a single monthly payment

Large funding amounts available

Considerations:

Higher monthly payment if you borrow more

Resets your mortgage term and interest rate

Closing costs apply

Tip: Only consider this if today’s rates are close to or lower than your current mortgage, or if you were planning to refinance anyway.

Final Thoughts: Match the Loan to the Project

There’s no one-size-fits-all answer. Here’s a quick summary of what to keep in mind:

Short, simple updates? Consider a personal loan or HELOC.

Major, one-time projects? A home equity loan offers stability.

Ongoing or uncertain costs? HELOCs offer unmatched flexibility.

Cash-flow sensitive? Equity-sharing avoids monthly payments.

Refinancing anyway? Explore a cash-out refi.

Whatever route you choose, be realistic about your budget, understand your repayment timeline, and talk to a trusted advisor before signing on the dotted line.

At Unison, our experts are here to help you find the right path forward. And for whatever makes the most sense for your situation, we can bring unique, innovative solutions to the table – with a focus on transparent, human-to-human service. We helped pioneer the equity sharing home loan, and now with HELOC/HELOAN products, we can help you access up to 90% of your home’s equity (up to $500,000) – with hassle-free closing, no usage restrictions, and no prepayment penalty. We’re able to consider FICO scores of 640+, and second properties can be eligible, too. Ready to find the right fit for your needs?

Disclaimer: This content is for informational and educational purposes only and does not constitute financial, legal, or lending advice. Loan terms and availability vary by lender and state. Consult a qualified financial professional or lender for personalized guidance tailored to your situation. Unison HELOC and Unison HELOAN are powered by SpringEQ and are not underwritten by Unison Mortgage Corp.