If you’ve built up equity in your home and are looking to tap into it, you’ve likely come across three common options:

HELOC (Home Equity Line of Credit)

HELOAN (Home Equity Loan / Second Mortgage)

Cash-Out Refinance

Each of these tools can help you access cash from your home, but they work in very different ways. The best choice for you depends on how much equity you have, what you’re using the funds for, and whether you want to replace your current mortgage – or keep it locked in.

Let’s break them down.

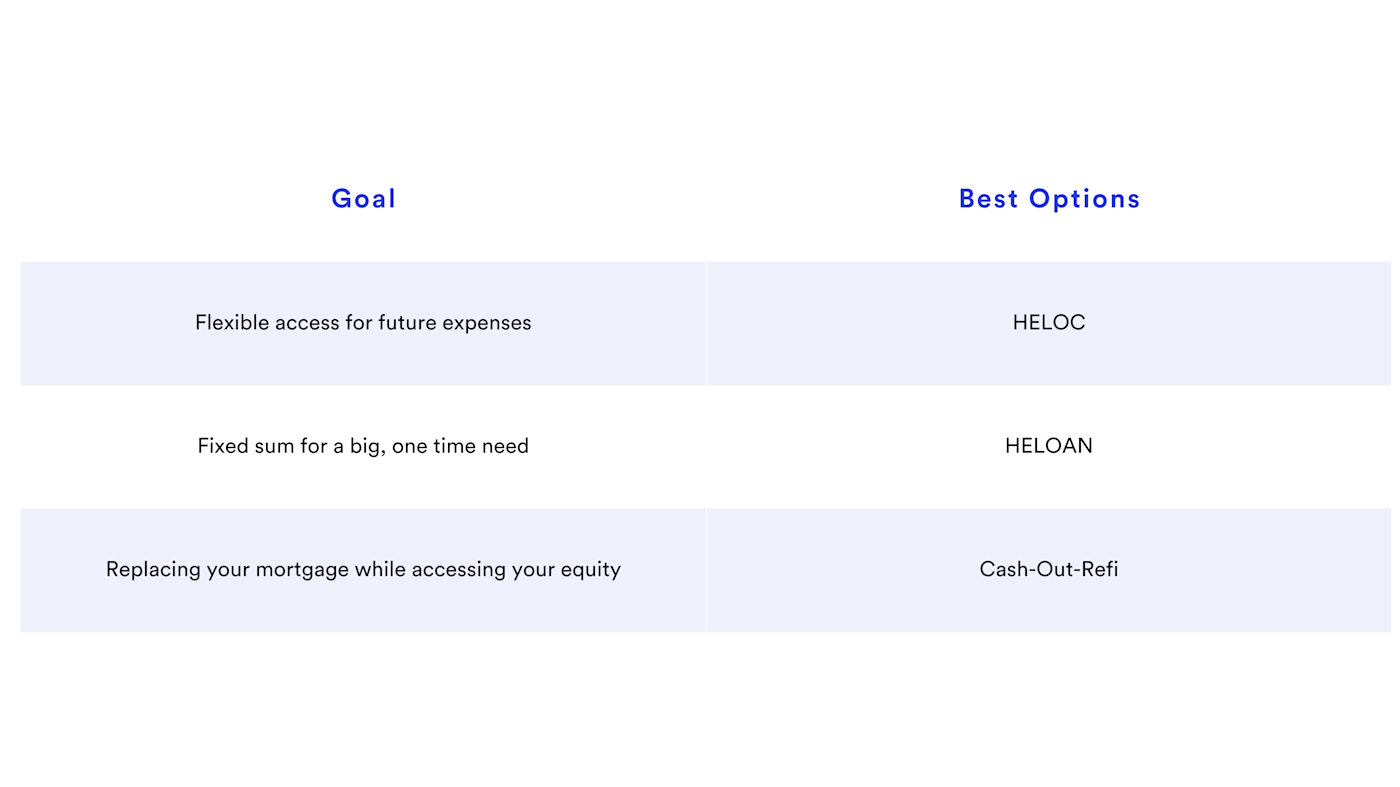

Option 1: HELOC (Home Equity Line of Credit)

A HELOC is a revolving line of credit (similar to a credit card) backed by your home equity. You can draw from it as needed, typically during a 5-10 year draw period.

Best For:

Ongoing or uncertain expenses (like phased home renovations)

Emergency backup funds or flexible access to capital

Borrowers who want to preserve their current mortgage

Key Considerations:

Most HELOCs tend to have variable interest rates, which can rise over time

Payments are usually interest-only during the draw period

Your home is used as collateral, so missed payments can have serious consequences (including foreclosure)

Tip: If you're considering a HELOC, have a plan for what you'll borrow and how you'll repay it, especially when the draw period ends.

Option 2: HELOAN (Home Equity Loan / Second Mortgage)

A HELOAN is a lump-sum loan that uses your equity as collateral. It has a fixed rate, fixed term, and fixed monthly payment, much like your original mortgage.

Best For:

One-time expenses (major renovations, medical bills, debt consolidation)

Borrowers who want predictable payments and interest rates

People who want to keep their current first mortgage in place

Key Considerations:

You'll pay interest on the full loan amount, regardless of how you use it

Rates are typically higher than a first mortgage, but lower than unsecured debt

It adds a second monthly payment alongside your existing mortgage

Tip: This option offers stability. It’s a good fit if you know exactly how much you need and want to lock in a monthly payment with zero surprises.

Option 3: Cash-Out Refinance

A cash-out refi replaces your existing mortgage with a new, larger loan. You “cash out” the difference between what you owe and what your home is worth.

Best For:

Those with a high mortgage rate looking to refinance anyway

Large funding needs that justify a full mortgage reset

Borrowers with strong credit and high equity

Key Considerations:

You’ll pay closing costs on the full loan amount, not just the cash-out portion

Extends or resets your loan term

May raise your monthly mortgage payment, depending on your new rate

Tip: A cash-out refi can be a win if current rates are lower than your existing mortgage, or if you're consolidating high-interest debt into a single payment.

So, Which One Should You Choose?

Your Equity, Your Strategy

Your home equity is a powerful tool. But like any financial product, these options all come with trade-offs. The best fit depends on your comfort with interest rates, your timeline, and how you plan to use the funds.

While HELOCs, home equity loans, and cash-out refinances are among the most popular ways to tap into your equity, they’re also not the only options out there. Product availability can vary from lender to lender, and in recent years, more innovative solutions like equity sharing home loans have emerged – offering alternative ways to access your equity without taking on additional debt.

As always, take time to compare your options, run the numbers, and think long-term. A well-matched solution can turn your home equity into a smart, strategic asset – not a financial burden.

At Unison, our experts are here to help you find the right path. And for whatever makes the most sense for your situation, we can bring unique, innovative solutions to the table – with a focus on transparent, human-to-human service. We helped pioneer the equity sharing home loan, and with our HELOC/HELOAN products, we can help you access up to 90% of your home’s equity (up to $500,000) – with hassle-free closing, no usage restrictions, and no prepayment penalty. We’re able to consider FICO scores of 640+, and second properties can be eligible, too. Ready to find the right fit for your needs?

Disclaimer: This content is for informational and educational purposes only and does not constitute financial, legal, or lending advice. Loan terms and availability vary by lender and state. Consult a qualified financial professional or lender for personalized guidance tailored to your situation.

Unison Mortgage Corp NMLS ID 2574289